The last four years since the repeal of PASPA have seen 30 states legalize sports betting, with 21 of them bringing online betting to their residents. The market has been quickly seized upon by industry heavyweights like DraftKings, FanDuel, Caesars, and BetMGM, among others.

These massive firms have spent stunning figures on customer acquisition and, in many states, licensing costs.

This begs the question about what it takes for a company to compete in the sports betting industry and the significant barriers newcomers face.

Cost of Admission

While sports betting licensing costs vary from state to state, nearly all available markets require significant sums to get started processing wagers. In addition to gaming licenses, operators are tasked with building sophisticated technology and achieving serious levels of compliance to ensure their products abide by standards each state imposes.

On top of these requirements, the average customer acquisition costs in sports betting are astronomical. Estimates put the cost of acquiring a new customer over $350-$400 per user, with DraftKings publicizing in 2020 that their average CAC was $371 (via Front Office Sports).

Caesars CEO Tom Reegs discussed in Squak Box the significant upfront costs the company faced in New York upon the recent launch.

It shocks no one that states are taking this opportunity to capitalize on eager operators with high license fees, taxation, and compliance. After all, the tax revenue states are generating from legal wagering is significant — over $1.5 billion since the repeal of PASPA in 2018.

However, with major players like DraftKings and FanDuel taking advantage of their vast assets to expand quickly, smaller operators can be restricted to pursuing smaller and fewer markets in attempts to gain ground and acquire some market share.

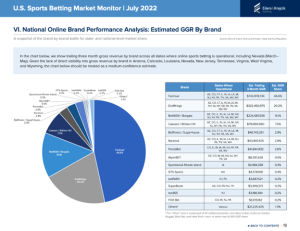

States such as New York ($25 million for 10 years), Illinois ($20 million), and Pennsylvania ($10 million) command massive licensing fees for operators to get started. Only a select few operators operate in all three of these states – DraftKings, FanDuel, BetMGM, Caesars, BetRivers, and PointsBet.

Market Consolidation

Collectively, these six sportsbooks make up 93.9% of the market share in the US per Eilers & Krejcik Gaming’s July 22 market share report. If the high barrier to enter these markets is limited to only the most financed of operators, smaller operators have little hope in their pursuit.

New York, Illinois, and Pennsylvania may be the most expensive licenses in the country only for a short time longer. California voters have a chance in November to approve two different proposals legalizing sports betting. One of them, Prop 27, would legalize online sports betting and allow commercial operators to partner with tribal casinos. The proposal would also see licensees pay a one-time $100 million fee, complemented by a $10 million renewal fee after every five years. The proposal would have lower requirements for tribes, charging a $10 million one-time fee and a $1 million renewal fee every five years.

Large operators are massive backers of this proposed legislation. DraftKings, FanDuel, Penn Entertainment/Barstool, BetMGM, Bally’s Interactive, Fanatics, and WynnBet all have joined in a coalition to spend tens of millions of dollars to support California’s legalization efforts. The inclusion of Fanatics and Penn in this coalition is noteworthy, signaling both operators see California as a pricey but worthy investment.

With lobbying so entrenched in the industry by the operators that can afford it, it is hard to predict we will see the trend start to move in favor of smaller operators.

On the Outside Looking in

Penn National owns about a 2.8% market share, operating in Pennsylvania, Michigan, Colorado, Indiana, Colorado, Virginia, New Jersey, and Arizona. The acquisition of Barstool Sports and rebranding of their digital product to Barstool Sportsbook was met with high expectations upon announcement. After a rocky start, Barstool’s high-profile media personalities and Penn’s industry experience fueled the firm to a record quarter in Q1 2022 with $1.6B in revenue, up 23% YoY. Their investment in Barstool, which will result in a complete ownership takeover by 2023 now that Penn has exercised its right to purchase all remaining stock, is proving to be a promising one.

By all accounts, Penn is a serious player in the gaming space. Yet despite the company’s momentum, it was unable to secure a New York license in a joint bid with Fanatics and Kambi.

Fanatics reportedly was planning for New York to be its inaugural product launch state. Fanatics Betting and Gaming has built a formidable team, with former FanDuel CEO Matt King taking over in the same role. King is joined by Ari Borod, former COO of The Action Network, and Scot McLintic, former Chief Product Officer at Penn. Fanatics CEO Michael Rubin is bullish on his firm’s ability to acquire market share once the product launches, claiming that Fanatics can be the No. 1 sportsbook in the US in 10 years. A launch date and initial market for the product remain unannounced at this time.

Penn and Fanatics make up two of the higher profile midsize operators (or future operators) in the space, joined by PointsBet, which owns approximately 2.6% of the national market share in line with Penn.

PointsBet operates in Colorado, Illinois, Indiana, Iowa, Michigan, New Jersey, New York, Pennsylvania, West Virginia, and Virginia. The trifecta of New York, New Jersey, and Pennsylvania is an expensive price to pay for their mid-size market shares. However, the Australian firm is looking to expand its North American businesses with a recent investment of $65M from the Susquehanna International Group announced in June of this year. This investment signals that PointsBet is unlikely to sell to a larger operator and instead pursue expansion in the top markets it is already operating in.

The nationally iconic brand of Sports Illustrated has partnered with European powerhouse 888Holdings in a joint venture aiming to bring consumer betting to SI’s 80+ million readers. SI Sportsbook operates in Colorado and Virginia, with several more states expected this year and early 2023. SI Sportsbook is brand new and needs time before true evaluations can be made of its performance. Its presence in the gaming space and strong brand recognition is an interesting test of consumer interest in the US market. The debut of SI Sportsbook is expected in New Jersey in the near future, but the joint venture with 888 is not expected to debut in NY, California, or other top markets in the near future.

Capital Restrictions

The ability to compete as an industry giant in gaming relies heavily on availability of capital, a fact reinforced by high customer acquisition costs and astronomical state licensing fees being the norm. It is hardly surprising states are taking this opportunity to generate significant new revenue streams.

Prop 27 in California would see 85% of the state’s revenue from gambling go towards helping the homelessness issue in the state. The time for states to convert their valuable sports markets into revenue is clearly upon us.

The obvious economic reality of a highly regulated space like gaming is that barriers to entry will be stacked against any newcomers. Startup operators seeking to offer differentiated products like Sporttrade, Wagr, and other ambitious companies have to deal with the fact that serious growth may be restricted to partnerships, acquisitions, or royalties. While every industry benefits from innovation and healthy competition, sports betting is unlikely to offer shortcuts to smaller operators or startups any time soon.

image by: sutadimages